One Inc Named to CNBC’s Top 500 Global Fintechs for Third Straight Year

Natural catastrophes caused estimated global insured losses of USD 105 billion in 2021, the fourth highest since 1970.1 The recording breaking volume and severity of weather-related events in 2021 wreaked havoc on P&C underwriting results, cut into insurer profitability, and impacted the cost of reinsurance. According to SwissRe, climate change is the key driver of a riskier and more complex property portfolio for insurers.2 With the two costliest natural disasters of 2021 recorded in the US, financial losses from climate risks will continue to greatly impact P&C insurers into 2023 and beyond.

The Earth’s climate is warming. According to NASA3, that’s the scientific consensus. Temperature data shows that global temperatures have warmed rapidly in recent decades. In many parts of the country, climate change is already creating an insurance crisis.

Since 1880, the Earth’s temperature has increased by 0.14° Fahrenheit per decade, according to NOAA4. Since 1981, the rate of warming has more than doubled, reaching 0.32° Fahrenheit per decade. These temperature increases may not seem like much, but the cumulative effect can be significant. According to USGS5, higher global surface temperatures will likely lead to more droughts and more intense storms. At the same time, rising sea levels will expose more locations to the erosive effects of ocean waves and currents.

Global warming can also contribute to wildfires. The EPA6 says that multiple studies have found that climate change has already caused longer and earlier wildfire seasons, larger burned areas and increased wildfire frequency.

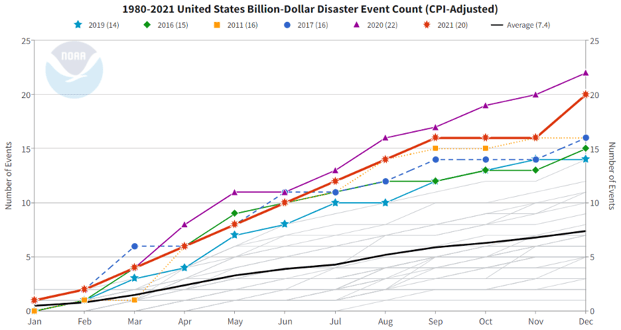

NOAA7 keeps track of weather and climate events with losses that exceed $1 billion, and the results are CPI-adjusted. The number of these billion-dollar events has increased dramatically in recent years. 2021 was the seventh consecutive year with 10 or more separate billion-dollar events. Between 1980 and 2021, the average number of events was only 7.4. Between 2017 and 2021, the average number of events jumped to 17.2 In 2021, there were 20 separate billion-dollar events, and the losses from these disasters total $145 billion. NOAA states that the higher number of billion-dollar events seems to hint at a new normal.

Month-by-month accumulation of billion-dollar disasters for each year on record. The colored lines represent the top 6 years for most billion-dollar disasters. All other years are colored light gray. NOAA image by NCEI. Source: https://www.climate.gov/media/13977

Wildfires have also broken records. According to U.C. Davis8, there were close to 9,900 wildfires in California in 2020, these fires burned 4.3 million acres – more than double the previous record.

Although property insurance rates have been rising around the country, some regions have seen particularly steep rate hikes. Faced with surging losses, insurers are pulling out of markets entirely.

According to Property Casualty 3609, an agent in New Orleans has reported premium hikes of double or even triple. Costly storms in recent years have caused some carriers to declare insolvency, and several insurance companies canceled more than 80,000 policies.

Florida has experienced similar problems. In a July 2022 article, Property Casualty 36010 reported that Citizens Property Insurance Corporation – the insurer of last resort for Florida property owners – could have 1.2 million customers by the end of 2022. At a meeting of its Board of Governors, Citizens CEO Barry Gilway said “the market is probably 75 percent shut down.” Multiple insurers have closed to new business, while others have added strict underwriting restrictions and rate increases.

Meanwhile, over on the West Coast, the California Department of Insurance11 has issued one-year moratoriums that prevent homeowners insurance companies from canceling or not renewing residential insurance policies in areas that are within or adjacent to the perimeter of a fire that has resulted in a declaration of a state of emergency.

We are already experiencing the effects of climate change from increasing temperatures and rising sea levels. Natural disasters are becoming more frequent and more severe, and the resulting losses are creating a crisis for both insurance companies and their policyholders.

Insurance leaders cannot assume that the recent spikes in storms, flooding and wildfires are an anomaly. Instead, this may be the new normal, and that means that insurance companies must quickly adapt. As weather events become more severe, insurers will be called upon to develop new insurance solutions and manage increasingly urgent claims scenarios.

Stay tuned for our upcoming blog article “How Insurers and Policyholders Can Navigate Climate Change’.

In a time of crisis, One Inc understands the challenges insurers and their customers face. After a disaster, insurers need to get money to their policyholders in real need, in real-time. Fire, wind, hail, and water can all wreak havoc quickly. We help you deliver fast and secure claim payments to your insureds via their preferred payment method and channel, no matter the situation. One Inc helps you get your customers back on their feet as quickly as possible.

Contact us to learn more.

Sources:

The One Inc Content Team strives to provide valuable insights about digital trends and payments innovation for the insurance community.