| By Chris Piwinski

One Inc Named to CNBC’s Top 500 Global Fintechs for Third Straight Year

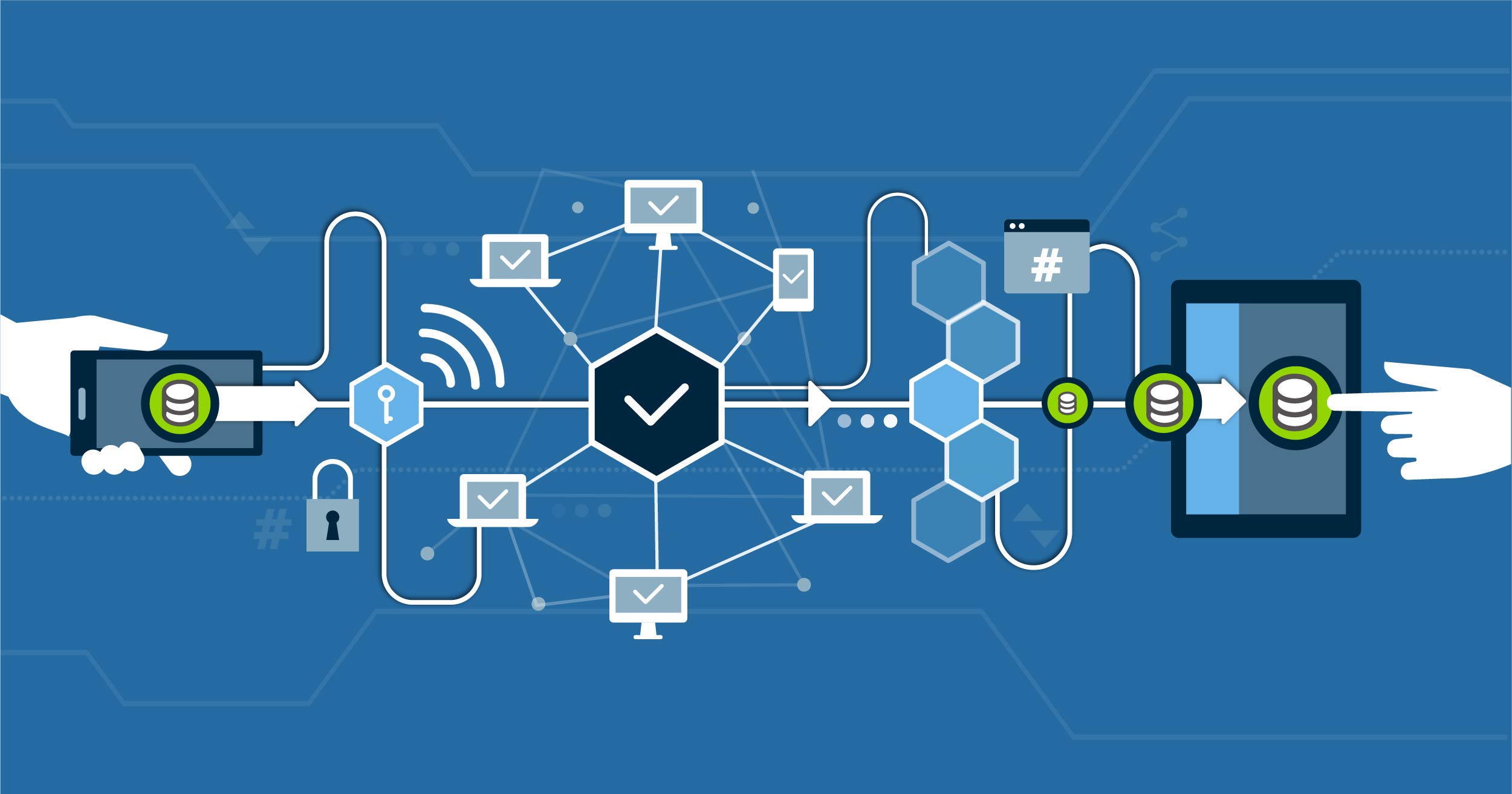

In part one of this two-part article, we looked at the basics of blockchain and its potential impact on the insurance industry. In part two, we’ll explore key areas for possible use cases, as well as issues and limitations for this growing technology.

As the insurance industry considers the best way to use blockchain, many companies will test the waters before deciding whether to jump into the deep end. The fact is, blockchain is a big undertaking, requiring careful consideration of the benefits, limitations, and areas in which it can improve processes.

Possible Use Cases for Blockchain in Insurance

Possible Use Cases for Blockchain in InsuranceThe following are key areas in which blockchain can be used to support the insurance industry.

![]() Improving underwriting processes. Transparency and the ability to verify data from a trusted source helps to reduce the number of communications among underwriters, brokers, and clients, and facilitate the underwriting process.

Improving underwriting processes. Transparency and the ability to verify data from a trusted source helps to reduce the number of communications among underwriters, brokers, and clients, and facilitate the underwriting process.

![]() Strengthening fraud detection and prevention. Blockchain’s decentralized ledger maintains a historical record that can be used to verify customers, policies, and transactions.

Strengthening fraud detection and prevention. Blockchain’s decentralized ledger maintains a historical record that can be used to verify customers, policies, and transactions.

![]() Streamlining claim processing. Quickly and accurately submit, process, and verify claims, eliminating processing delays and manual efforts.

Streamlining claim processing. Quickly and accurately submit, process, and verify claims, eliminating processing delays and manual efforts.

![]() Solidifying customer trust. Improve customer engagement and trust with streamlined onboarding, instant verification of customer documents and identity, real-time customer service requests, and more.

Solidifying customer trust. Improve customer engagement and trust with streamlined onboarding, instant verification of customer documents and identity, real-time customer service requests, and more.

![]() Simplifying reinsurance. Improve efficiencies and reduce unnecessary expenses and erroneous payouts.

Simplifying reinsurance. Improve efficiencies and reduce unnecessary expenses and erroneous payouts.

Blockchain’s Issues and Limitations

Blockchain’s Issues and LimitationsWhile experts predict that blockchain can be a real game changer for the insurance industry, the technology isn’t without its challenges. In fact, in these early stages of development, blockchain has its limitations and isn’t always appropriate for many types of digital interactions. Issues of concern currently associated with blockchain include:

![]() Capacity and scalability. One of blockchain’s key benefits is its potential for storing large amounts of data in each block. However, as transaction and record volumes increase, systems may not have the ability to scale fast enough to keep up with the demand.

Capacity and scalability. One of blockchain’s key benefits is its potential for storing large amounts of data in each block. However, as transaction and record volumes increase, systems may not have the ability to scale fast enough to keep up with the demand.

![]() Lack of standardization. According to Deloitte Insight’s Tech Trends, companies looking to adopt blockchain capabilities currently have no established best practices or overarching technical standards to follow.

Lack of standardization. According to Deloitte Insight’s Tech Trends, companies looking to adopt blockchain capabilities currently have no established best practices or overarching technical standards to follow.

![]() Slow response times. As transactions and data volumes increase, the number of blocks will grow, making the blockchain longer. This can create a potential backlog, delaying the verification process.

Slow response times. As transactions and data volumes increase, the number of blocks will grow, making the blockchain longer. This can create a potential backlog, delaying the verification process.

![]() Initial costs. Blockchain applications will require users to upgrade or, in some instances, even replace their legacy platforms. For many, the initial investment of time and money to make the migration may not be feasible.

Initial costs. Blockchain applications will require users to upgrade or, in some instances, even replace their legacy platforms. For many, the initial investment of time and money to make the migration may not be feasible.

![]() Human error. As with a traditional database, information stored on the blockchain must be high-quality and recorded accurately at the time of entry. Unfortunately, blockchain’s inalterability (meant to help protect records from being tampered with) may be an impediment, preventing correction of inaccuracies caused by human errors.

Human error. As with a traditional database, information stored on the blockchain must be high-quality and recorded accurately at the time of entry. Unfortunately, blockchain’s inalterability (meant to help protect records from being tampered with) may be an impediment, preventing correction of inaccuracies caused by human errors.

Technology for Legacy Systems

Technology for Legacy Systems As the insurance industry spreads its technology wings, some companies may find the adoption of new tech processes overwhelming, particularly when it comes to integration with legacy systems. For those looking to make changes, blockchain may be just too big a slice of the technology pie to take on at the moment.

In Deloitte’s Tech Trends 2018, it’s recommended that insurers first determine whether their company actually needs what blockchain offers. And, while blockchain can be a powerful tool, it is only applicable in certain use cases, making it critical to understand the extent to which blockchain can support key business strategies and drive value.

Remember, adopting new technologies doesn’t have to be an all-or-nothing proposition. Sometimes it can be to your advantage to take the modernization of processes in a series of smaller, more manageable steps.

The Insurer's Guide to Going Digital

Want to know more about how insurers are using blockchain and other digital solutions today? Download the the eBook for the latest tech trends in insurance!

#GoDigital

You might also be interested in:

Chris Piwinski is a Product Marketing Manager at One Inc, focusing on “what’s now” and “what’s next” in insurance technology.